Some of our clients enjoy keeping up with how markets have been behaving, while others prefer to focus on their long‑term plans rather than short‑term movements. Whichever camp you fall into, this quarterly commentary provides a snapshot of what has been happening across global markets and the factors influencing investment performance.

It’s worth remembering that no single quarter tells the whole story, long‑term goals, diversification, and staying invested remain far more important than any short‑term market changes. But for those who like to stay informed, the following highlights summarise the main themes from the past three months.

This commentary is aimed at readers with an intermediate knowledge of investments, those familiar with concepts such as equities, bonds, and diversification, though anyone with an interest in markets may find it useful.

Key Moments of the Quarter

A challenging quarter for markets: Markets entered 2026 with optimism (easing inflation, solid growth), but sentiment shifted in Q1 due to renewed AI uncertainty followed by the rising geopolitical tensions, especially in the Middle East.

Geopolitics driving inflation risk: Conflict in the Middle East has threatened oil supply, pushing energy prices higher and raising inflation concerns, leading to higher bond yields and complicating central bank decisions.

Selective equity markets: Instead of broad gains, investors are focusing on company fundamentals, with a shift away from expensive growth stocks (especially tech/software) toward sectors benefiting from higher energy prices.

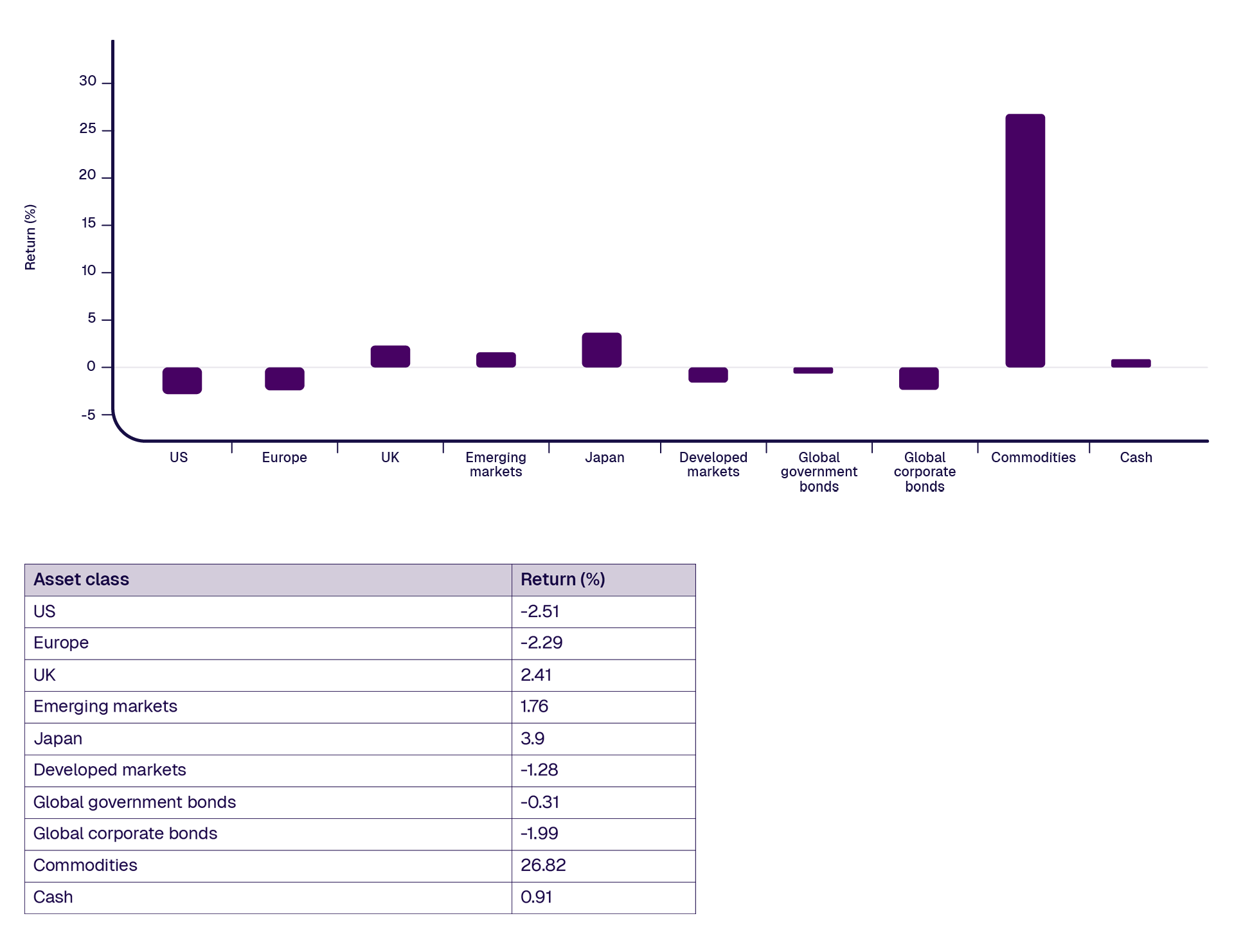

Diverging regional and asset performance: Energy-linked markets (like the UK) held up better, while energy-importing regions struggled; bonds fell as yields rose, and gold declined despite uncertainty due to a strong US dollar and profit-taking.

Uncertain but cautiously optimistic outlook: While short-term volatility and risks remain elevated, corporate earnings are broadly resilient, and long-term growth drivers persist, making diversification and a long-term investment approach key.

Asset Class Returns Q1 2026

Source: FE Analytics. US: S&P500, Europe: MSCI Europe ex. UK, UK: FTSE 350, Emerging Markets: MSCI Emerging Markets, Japan: TOPIX, Developed Markets: MSCI World, Government bonds: Bloomberg Global Treasury, Corporate bonds: Bloomberg Global Aggregate – Corporate, Commodities: Bloomberg commodities index, Cash: BoE Sterling overnight index average. All Indices are hedged back to pounds sterling.

At the start of 2026, financial markets were carrying strong momentum. Inflation had been easing gradually, economic growth remained resilient, and many investors appears optimistic, although views were not uniform.

However, the first quarter of the year has challenged that positive outlook. Two key developments have driven this shift. First, renewed concerns around artificial intelligence have created uncertainty about future growth and investment. Second, rising tensions in the Middle East have added a new layer of geopolitical risk.

The situation in the Middle East is particularly important for markets because it affects the supply of oil. When oil supply is disrupted, prices may rise, which can contribute to higher inflation over time, although this will also depend on demand conditions and policy responses. This shift in expectations is already being reflected in bond markets, where yields have increased as investors demand higher returns to compensate for the risk of inflation staying elevated. This has also made the path forward less clear for central banks, which must balance controlling inflation with supporting economic growth. At the same time, uncertainty around global trade has increased.

Equity markets have felt the impact as well. Rather than broadly rising, markets have become more selective. Investors are now focusing more closely on the fundamentals of individual companies, particularly their ability to generate consistent cash flow and demonstrate real value.

As things stand today, there is a temporary two-week ceasefire between the United States and Iran, offering a short pause in tensions. However, uncertainty remains high in the near term.

Some of the Investment Managers we speak with remain optimistic about the long-term and the businesses they are invested in. However, it is important to recognise that while markets are reacting to these developments, the outcome is still unclear. For now, investors are navigating a more uncertain environment, where both risks and opportunities are evolving.

Equities

Global equity markets faced a more difficult environment over the first quarter of 2026, with performance varying significantly across sectors and regions.

One of the key themes early in the quarter was a shift away from higher-growth areas of the market, particularly software businesses, as investors began to question the price of these businesses. This rotation was driven by several factors, however. Rising bond yields made future earnings less attractive in today’s terms, while changing expectations around inflation and interest rates added further pressure. At the same time, investors are grappling with which companies are likely to emerge as the long-term winners of the AI race.

However, a key driver of markets was the conflict in the Middle East. In late February, coordinated military strikes by the United States and Israel on Iran significantly escalated tensions. This led to disruption in the Strait of Hormuz, a critical route for global energy supply, and pushed oil prices higher.

Higher energy prices provided a boost to energy and commodity-linked companies. UK equities were relatively resilient, partly reflecting their higher exposure to energy and commodity-linked sectors. In contrast, regions such as Europe and Emerging Markets, which are generally net importers of energy, faced greater challenges as rising costs put pressure on both economic growth and household spending. At the time of publication, a temporary two-week ceasefire is in place, but the longer-term outlook remains uncertain. This is reflected in investor sentiment, which continues to be cautious. Geopolitical risks are feeding into expectations for growth and central bank policy, and while corporate earnings have remained broadly resilient, persistently higher inflation could weigh on future profitability.

In Japan, a victory for the Liberal Democratic Party in a snap election raised expectations of policies supportive of economic growth. This provided a tailwind for Japanese businesses for the quarter.

In the US, overall equity performance was weighed down by weakness in the technology sector, as mentioned earlier. Given the significant size of these companies within the market, their underperformance had a disproportionate impact on overall returns. However, this does not reflect the full picture. Many companies performed well over the quarter, with more than half of the stocks in the S&P 500 delivering positive returns. Strength was particularly evident in sectors such as Energy, Materials and Utilities, which benefited from the broader market environment.

Bonds

At the start of the year, investors were anticipating interest rate cuts from both the Federal Reserve and the Bank of England in 2026. However, this view shifted significantly as the quarter progressed. As concerns around rising inflation peaked, markets began to reprice the outlook for interest rates, moving away from expected cuts towards a “higher for longer” scenario, with some even considering the possibility of further rate increases. While this adjustment may prove to be overdone, it highlights how quickly sentiment has changed and suggests a more cautious stance from central banks.

This shift had a direct impact on bond markets. When expectations for inflation and interest rates rise, bond yields also rise, and because bond prices move in the opposite direction to yields, this led to declines in bond prices. Across major markets such as the US and UK, yields moved higher over the quarter, reflecting this shift.

Gold

The first quarter of 2026 served as a reminder that markets do not always behave in line with investor expectations. In periods of geopolitical uncertainty, gold is often viewed as a safe haven, providing diversification. However, despite the rising uncertainty and tensions in the middle east, gold prices actually fell from their highs seen in 2025.

Several factors contributed to this weakness. A stronger US dollar reduced the attractiveness of gold for international investors, while the asset’s strong performance in the prior year also led to some profit-taking as volatility increased.

Overall, the move highlights the difficulty of timing markets and reinforces the importance of being prepared for a range of possible outcomes rather than relying on any single expected scenario.

Outlook

Looking ahead, the key feature of markets is a higher level of uncertainty across almost all asset classes. Geopolitical tensions, shifting inflation expectations, and questions around the long-term impact of artificial intelligence have all contributed to a more complex and less predictable environment for investors.

Importantly, while short-term conditions have become more volatile, the underlying picture for many companies and economies remains broadly intact. Corporate earnings have generally held up, and investment managers remain cautiously optimistic about the longer-term opportunities available in global markets.

For our clients, the key message is that uncertainty and volatility are likely to remain in the near term, but reacting to short-term noise could be detrimental in achieving long-term goals. Maintaining diversification and a long-term perspective are often an effective approach, although the appropriate strategy will depend on individual circumstances and objectives.

We know that market updates aren’t for everyone, and that’s perfectly fine. The purpose of this commentary is simply to give you a clearer understanding of some of the factors that professional investment managers consider when building and maintaining portfolios.

Nothing here is intended to guide personal investment decisions. Instead, these developments are monitored and interpreted by the investment managers behind your funds or model portfolios, who make changes where appropriate as part of a structured investment process.

If you’d like to understand how these themes relate to your longer‑term plan — or if you simply have questions — your Financial Planner is always ready to help.

Important Information

This commentary is for general information only and does not constitute personal financial advice. You should seek advice tailored to your individual circumstances before making any investment decisions. Past performance is not a reliable indicator of future results. Investments can go down as well as up. You may get back less than you invested.

Market conditions can change rapidly. The views expressed are based on current market conditions and may change without notice. Any estimates, forward‑looking statements or forecasts do not represent a guarantee of future performance. The information is not intended to be complete or exhaustive and no representations or warranties, either express or implied, are made regarding the accuracy or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the reader.

References to individual companies are for illustrative purposes only and do not constitute a recommendation to buy or sell.

Fidelius Ltd is authorised and regulated by the Financial Conduct Authority. Our FCA reference is 188615. Registered No. 03658809 ENGLAND. Registered Office: No.1 Bath Quays, 1 Foundry Lane, Bath, BA2 3GZ.